If I had to sum it up in one line: Medicaid brokers bring trip volume, while private pay brings more control and faster cash.

If you run a small NEMT fleet, this choice affects everything day to day:

- how rides get booked (often requiring specific dispatch software features for broker integration)

- how much paperwork you deal with

- how long you wait to get paid

- how much pricing control you keep

- how much claim or collection risk you take on

Here’s the short version:

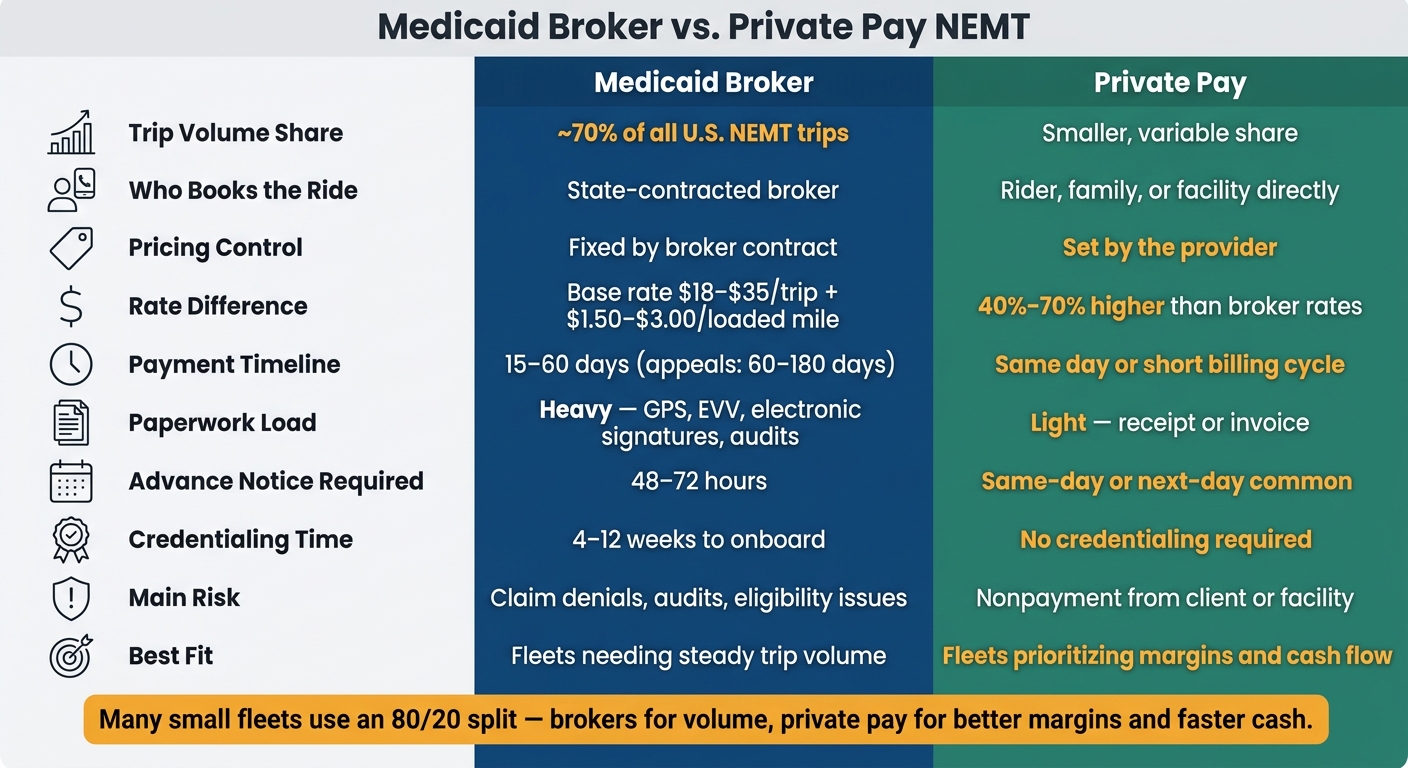

- Medicaid brokers handle about 70% of NEMT trips in the U.S.

- Broker work can keep vehicles moving, but rates are often 40% to 70% lower than private pay

- Broker payments may take 15 to 60 days

- Private pay usually means direct booking, simpler billing, and payment at the time of service or on a short billing cycle

- Private pay can bring better margins, but trip flow is less steady and you have to do your own selling and collecting

So the tradeoff is simple: volume vs. control, and steady trip flow vs. better cash timing.

Medicaid Broker vs. Private Pay NEMT: Key Differences at a Glance

Brokers vs Private Pay Clients for Your Non Emergency Medical Transportation (NEMT) Business

sbb-itb-af83355

Quick Comparison

| Criteria | Medicaid Broker | Private Pay |

|---|---|---|

| Who books the ride | Broker | Rider, family, or facility |

| Trip volume | Higher | Less steady |

| Pricing | Fixed by contract | Set by provider |

| Paperwork | Heavy | Light |

| Payment timing | 15–60 days in many cases | Often same day or short cycle |

| Risk | Claim denials, audits, eligibility issues | Nonpayment from client or facility |

| Best fit | Fleets that need steady trip flow | Fleets that want better margins and more control |

For many small operators, choosing the right cloud-based vs. on-premise NEMT software and finding the best mix is not all-or-nothing. A broker-heavy setup can fill the schedule, while private pay can help bring in better per-trip revenue and faster cash.

How Each Model Works Day to Day

The gap between these two models shows up almost right away in how a ride moves from request to payment.

Medicaid Broker Workflow

In the broker model, the trip starts with the broker, not the transportation provider. A Medicaid member contacts the state’s contracted broker, and that broker handles trip approval, eligibility checks, and authorization before the ride ever reaches a provider. Once approved, the provider gets the trip through the broker’s portal. If a company works with more than one broker, the team usually has to juggle multiple broker portals every day.

The split is pretty clear: the broker controls eligibility and trip assignment, while the provider handles the ride itself. Scheduling usually depends on 48 to 72 hours of advance notice, and trips are often grouped together to cut costs. That can lead to longer pickup windows and run times that are harder to predict.

Paperwork is tight. Drivers need to record GPS breadcrumbs, timestamps, and electronic signatures using specialized NEMT software. Claims are paid only after review and verification. Clean claims are usually paid in 15 to 45 days, and appeals can stretch from 60 to 180 days.

Private Pay Workflow

Private pay works in a much more direct way. The booking comes straight to the provider, with no broker portal and no prior authorization. The customer might be a family member, a senior, or a facility arranging a ride.

That gives the provider more control over pricing, dispatch, and collection. Rates are set by the provider, including mileage charges and wait-time add-ons. Documentation is light, often just a receipt or invoice. Payment is often collected at the time of service or billed to a facility on a short cycle.

The catch is simple: collection risk sits with the provider. Payment depends on the rider or facility paying on time.

Here’s the side-by-side view:

| Feature | Medicaid Broker | Private Pay |

|---|---|---|

| Advance Notice | 48–72 hours required | Same-day or next-day common |

| Ride Type | Often shared/multi-stop | Dedicated, direct |

| Documentation | GPS, EVV, electronic signatures | Receipt or invoice |

| Payment Timeline | 15–45 days after claim verification | Immediate or short facility cycle |

Those workflow gaps shape the day-to-day pressure points for small fleets, especially around compliance, cash flow, and scheduling.

Side-by-Side Comparison: Operations, Revenue, and Risk

Those workflow gaps create very different kinds of pressure. You see it fastest in paperwork, payment speed, and margin.

| Factor | Medicaid Broker | Private Pay |

|---|---|---|

| Who Pays | State Medicaid / third-party broker | Individual, family, or facility |

| How You Get Paid | Broker portals | Direct invoice, cash, or card |

| Trip Volume Stability | High – steady broker assignments | Variable – depends on marketing |

| Claim Risk | High – technical errors or eligibility issues | Low – payment is collected directly |

| Margin Potential | Lower – fixed contract rates | Higher – provider sets custom rates |

| Admin Complexity | High – credentialing, audits, portal management | Low – no insurance claims or third-party vetting |

Administrative and Compliance Differences

The biggest drag is compliance and onboarding. The more control brokers have, the more work lands on the provider before any money comes in.

Credentialing by itself can take 4 to 12 weeks, and one missing item can stop the whole thing cold. An expired background check or an insurance certificate that doesn’t list the broker as an "additional insured" is enough to stall approval. After activation, providers still have to track GPS "Arrive" and "Drop Off" timestamps within 300 feet of the pickup location to trigger payment, while also keeping driver files clean at all times.

Audit risk is not small. Between FY2015 and FY2020, the GAO documented about 200 criminal convictions and civil settlements tied to NEMT fraud, mostly around mileage inflation and "phantom rides". Private pay removes that layer. There’s no prior authorization and no third-party audits.

Revenue and Cash Flow Differences

The rate gap changes the business math. But timing matters just as much as price.

Private pay rates for the same transport are 40% to 70% higher than Medicaid broker rates for similar trips. Broker reimbursement for standard ambulatory trips usually falls between $18 and $35 per base trip, plus $1.50–$3.00 per loaded mile, with no reimbursement for deadhead miles. Private pay providers can build those costs into their own rates .

That’s where cash flow starts to pinch. A 60-day payment cycle can leave a fleet funding two months of operations before the money shows up. Private pay comes with its own risk – unpaid invoices instead of delayed reimbursements – but it gives providers more say over when cash hits the account.

What Both Stakeholders Need From NEMT Providers

Money and paperwork may differ, but both models look at the same thing in the end: service quality. Whether a trip is paid through a broker or by a private client, providers are still judged on being on time, handling riders with care, and keeping records clean and accurate.

Shared Service Expectations

Punctuality is non-negotiable on both sides. Broker contracts often require on-time performance of 95% or higher. Private pay clients expect that same level of dependability too, especially families trying to coordinate rides for aging parents.

Driver professionalism is another thing both sides care about. In brokered NEMT, drivers need proper credentials and background checks. On the private-pay side, clients look for a more high-touch experience, but the bar is still high.

Vehicle readiness matters in both models. Providers need to send the right vehicle for each rider’s mobility level every single time, whether that means ambulatory, wheelchair, or stretcher service.

Shared Operational Systems

Meeting those standards gets much easier when dispatch, tracking, and billing all run through one central setup. For small fleets, that same setup helps with broker compliance and gives private-pay clients the transparency they want. Centralized scheduling, GPS tracking, and digital billing support both payer types .

That shared baseline shifts the main decision to a few practical issues: fleet size, admin capacity, and cash flow.

Which Model Fits Your NEMT Operation Best

Best Fit by Fleet Size and Admin Capacity

Now that the workflow differences are on the table, the next step is simple: figure out which payer mix your fleet can actually handle right now.

The better fit usually comes down to three things: cash flow, admin bandwidth, and trip volume. Not the plan you hope to grow into next year. The setup you can support today.

New operators often need broker volume first. That steady flow of trips can keep vehicles moving, and some brokers offer faster payment cycles, which can help cover early operating costs before cash flow settles down.

For owner-dispatchers with 2–10 vehicles, the main job is keeping those vehicles booked. Broker relationships can help with utilization, but there’s a catch: portal work eats up time fast. When you’re already juggling dispatch, driver issues, and billing, that extra admin load adds up.

Tools like RouteGenie can take some of that pressure off. It connects with major brokers like ModivCare and MTM, pulls trips into dispatch, and syncs trip completion data back for automated billing.

Once a fleet has shown it can perform well with brokers, it can start adding private-pay trips and facility contracts. That shift can help margins and improve cash timing.

So the choice comes down to what matters most right now: volume, margin, or some middle ground.

Conclusion: Volume, Control, and Cash Flow

There’s no one-size-fits-all setup here.

Medicaid brokers handle about 70% of all NEMT trips in the U.S., so most fleets can’t just ignore that channel. At the same time, running on 100% broker volume can pile too much risk into one bucket, especially if a major source like ModivCare runs into financial trouble.

For many small fleets, a broker-heavy mix works best for volume, while private pay helps on margin. A common split is 80/20: brokers for steady trip flow, private pay for better margins and better cash timing.

The practical move is to look at your working capital, your billing capacity, and the broker setup in your area before you lean too hard in either direction.

FAQs

How do I decide on the right payer mix?

Balance your business goals with your day-to-day capacity and the market around you. Medicaid can bring a steady flow of high-volume demand, but it also comes with fixed rates, more paperwork, and slower payment. Private pay can mean better margins and faster payment, but demand may swing more, and you may need to spend more on marketing to keep leads coming in.

A lot of operators hedge their bets by mixing both. They use Medicaid to keep volume steady, then add private pay or facility contracts to help margins.

Which model is better for a new NEMT company?

It comes down to your goals and how much cash you have on hand.

A lot of new operators start with Medicaid brokers like ModivCare because they can provide a steady flow of trips. The tradeoff is pretty clear: Medicaid usually means more paperwork and payment cycles that can stretch from 30 to 90 days.

Private pay often brings higher margins and faster payments. But it can be less predictable, and you have to market your services to keep rides coming in.

Because of that, many operators move to a mixed model over time to help keep revenue more stable.

What are the biggest cash flow risks in each model?

Medicaid’s biggest cash flow risk is the long payment timeline. In many cases, providers wait 30 to 90 days to get paid. On top of that, there’s the claim filing work itself, plus delays that happen when documentation errors slip in.

Private pay is usually faster. Payment can come right away or within 30 days, which makes cash flow easier to manage. It also skips insurance claim denials. The trade-off is demand can be less predictable, so operators need steady marketing to keep volume consistent.